17a-13 Is a Procedure Test, Not a Paper Exercise

There is a quiet assumption inside a lot of compliance programs: that having a documented quarterly-count procedure is the same as passing on it. SEC Rule 17a-13 is built to test the opposite. The rule requires broker-dealers to physically count securities, verify positions open more than 30 days, compare the results against the firm's records, and record any unresolved differences within 7 business days. A binder that describes all of that is not the control. The control is the evidence that it actually happened, in order, on time.

That is the distinction examiners probe. Not "do you have a procedure," but "can you prove the procedure ran."

The Count Has to Prove Something

Most firms understand that the quarterly process exists. The harder question is what the process is supposed to prove. Rule 17a-13 exists to demonstrate that the firm knows what securities it holds, what is in transfer or transit, and what has been loaned, borrowed, failed to receive, or failed to deliver. The count is a reconciliation of records against reality. When a firm cannot produce the population, the count, the verification, and the difference log as one connected set, the reconciliation stops being provable — and an unprovable control is, for exam purposes, a missing one.

Why 30-Day Items Are the Pressure Point

The 30-day open position population is where the rule bites hardest. Those items require direct verification with the counterparty, so the firm has to identify them and then track the confirmations, the non-responses, and the follow-ups against a deadline. This is precisely where spreadsheet-and-inbox workflows fracture. The mailing may go out. The response may even come back. But if that evidence is scattered across email threads, PDF folders, and a side tracker, the record is thinnest at the exact moment it carries the most weight.

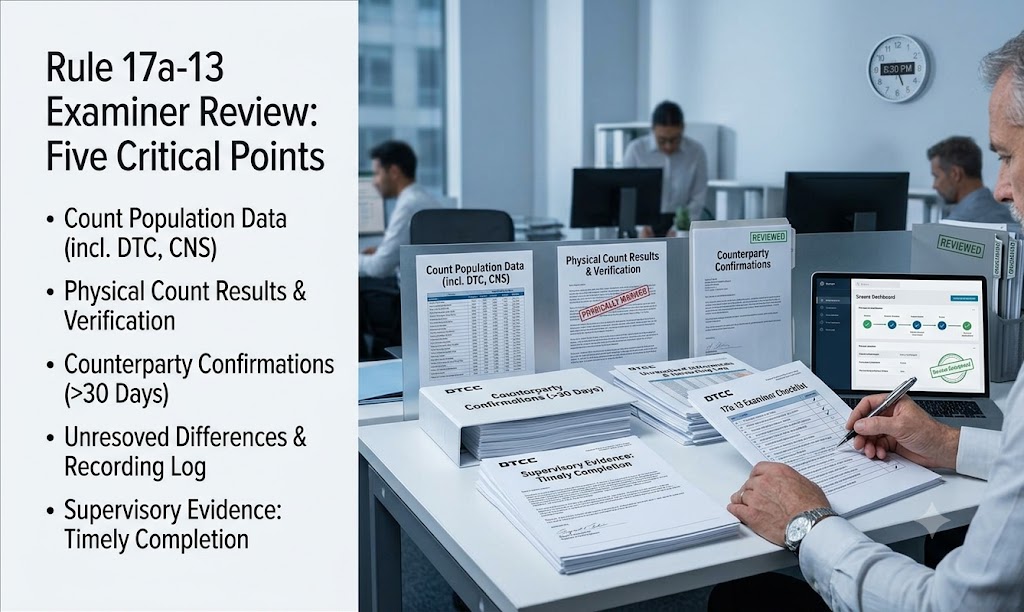

The Evidence Shape an Examiner Recognizes

A reviewer working through a 17a-13 process is generally looking for five connected records:

- The population included in the count.

- The results of the physical count or verification.

- The counterparty confirmations for positions open more than 30 days.

- The unresolved differences and how they were recorded.

- The supervisory sign-off showing the process finished on time.

Produced quickly and in sequence, that set makes the process look controlled. Recreated after the request lands, the same five records make it look improvised — even if the work was done correctly the first time.

Where QBS Fits

Quarterly Broker Statement (QBS) was built to keep that trail intact as the work happens. It automates the quarterly securities count and counterparty verification for borrows, loans, repos, and fails, and it tracks the 17a-13(b)(3) confirmation letters for positions open 30 days or longer — logging what was sent, what came back, and what still needs attention against the 7-business-day clock. The point is not that QBS mails letters faster. It is that the sending, the verification, and the difference handling are captured as one supervised record instead of assembled later from fragments.

When the Test Becomes About the Paper

When a quarterly count turns into a scramble, the cost lands in two places. Operations burns hours locating records and reconciling discrepancies. Then legal and management burn more hours defending the response and explaining where the evidence lived. The irony is sharp: a rule designed to test whether your records match your securities can collapse into an argument about where the paperwork went. The count itself may have been fine. If the trail is scattered, the exam story is still weak.

If your Rule 17a-13 process still runs on spreadsheets, mailed letters, and manual follow-up, the trail is the thing to fix first — before the next document request makes the point for you. Contact Loffa Interactive Group to tighten the workflow, strengthen the supervisory record, and meet SEC Rule 17a-13 with a count you can prove, not just describe.

Related reading: Why 30-Day Open Positions Create the Hardest Questions Under 17a-13.