Deciphering FINRA’s Fee Adjustments: Strategic Implications for Brokerage Firms

Navigating Through FINRA’s Latest Fee Adjustments: A Closer Look for Brokerage Firms

Introduction

With the financial industry in a constant state of evolution, especially concerning regulatory compliance and associated costs, the announcement from the Financial Industry Regulatory Authority (FINRA) regarding an adjustment in fees has stirred the financial community. Loffa Interactive Group, standing at the forefront of blending technology and financial service solutions, acknowledges the potential ripple effects of these fee adjustments on our clients and the wider financial sphere.

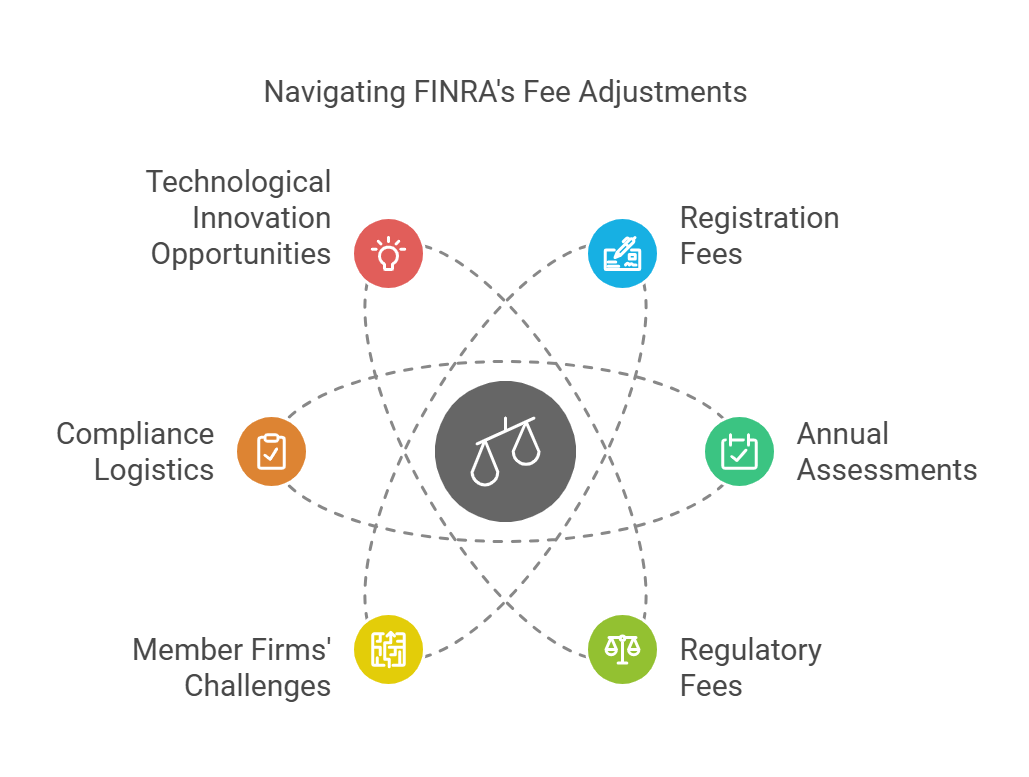

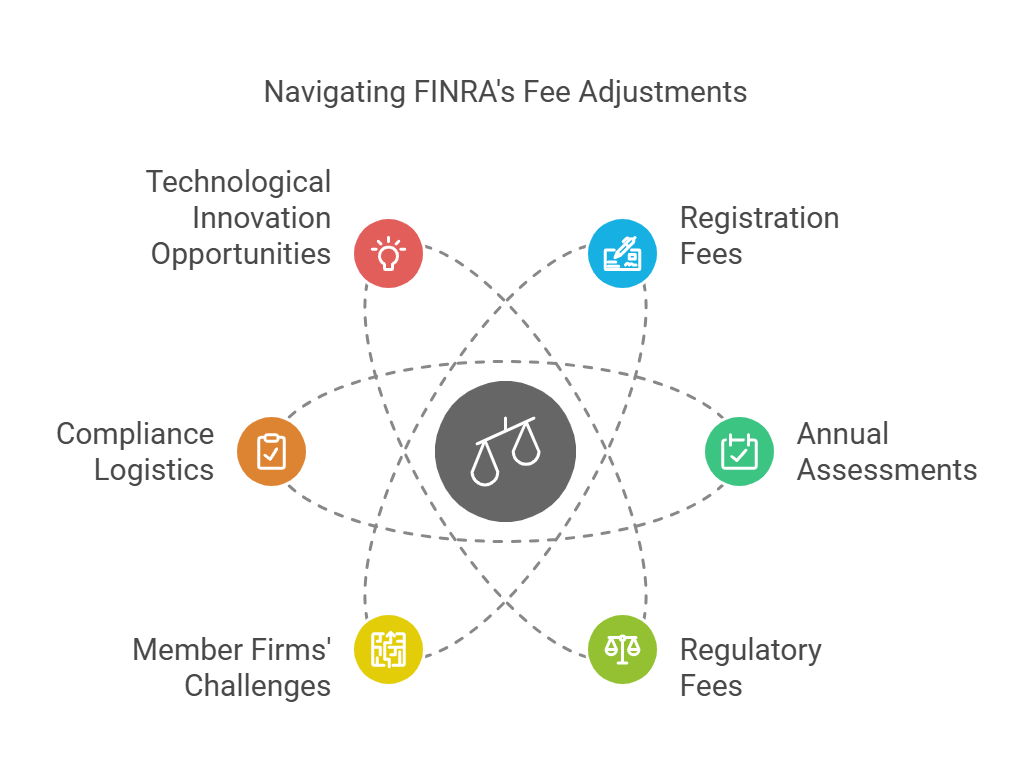

Understanding the Fee Adjustments

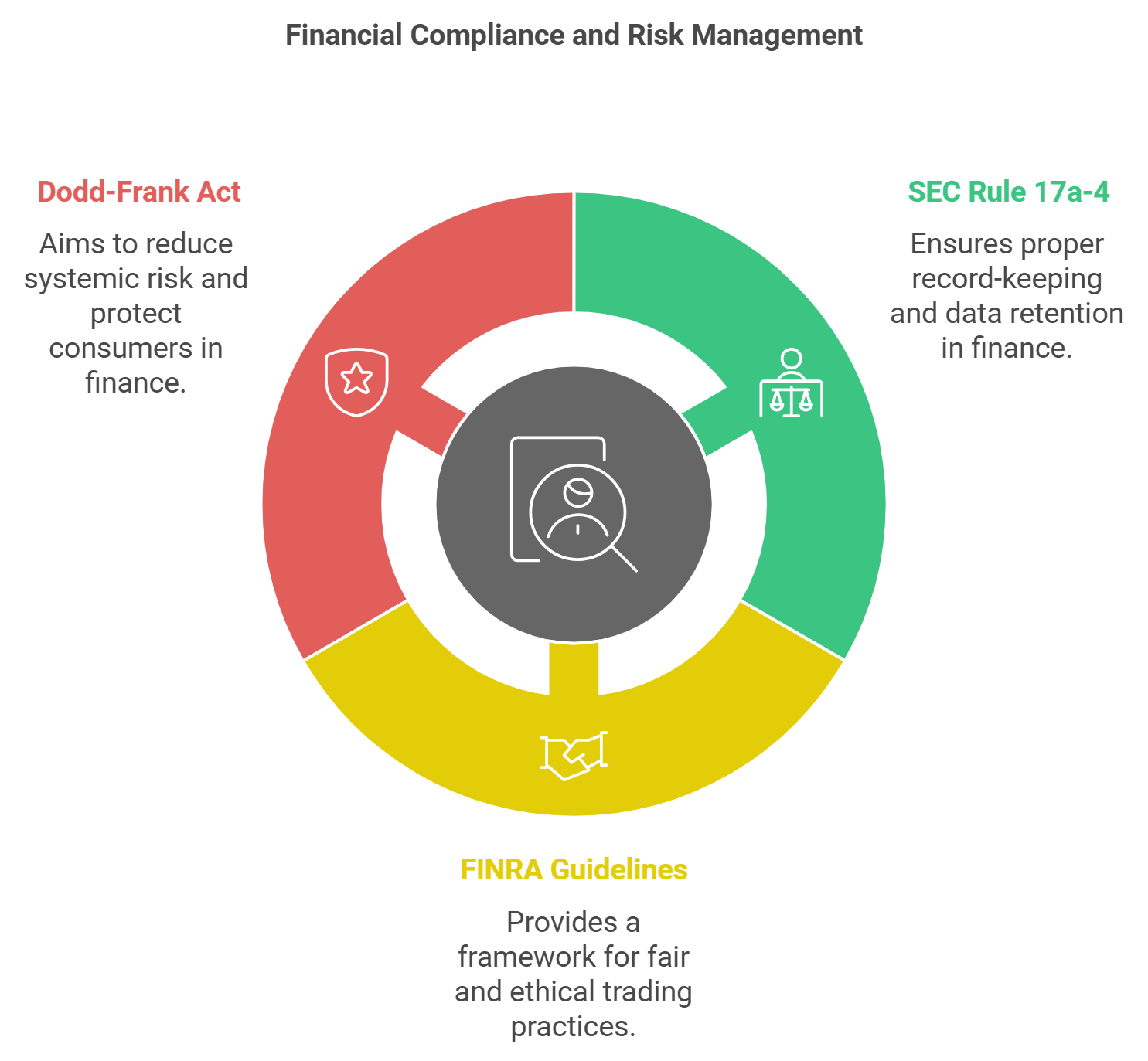

FINRA’s decision to adjust fees encompasses various operational fees, including but not limited to registration, annual assessments, and regulatory fees. These adjustments are aimed at fortifying FINRA’s regulatory prowess, ensuring it continues to safeguard investor interests and uphold market integrity efficiently.

The Dual-Edged Sword

For member firms, interpreting these fee adjustments translates into navigating a landscape sprinkled with challenges and opportunities. On one side, the tug on operational budgets might seem daunting, compelling a reassessment of compliance logistics. On the flip side, it presents a remarkable opportunity to redefine compliance strategy through the lens of technological innovation.

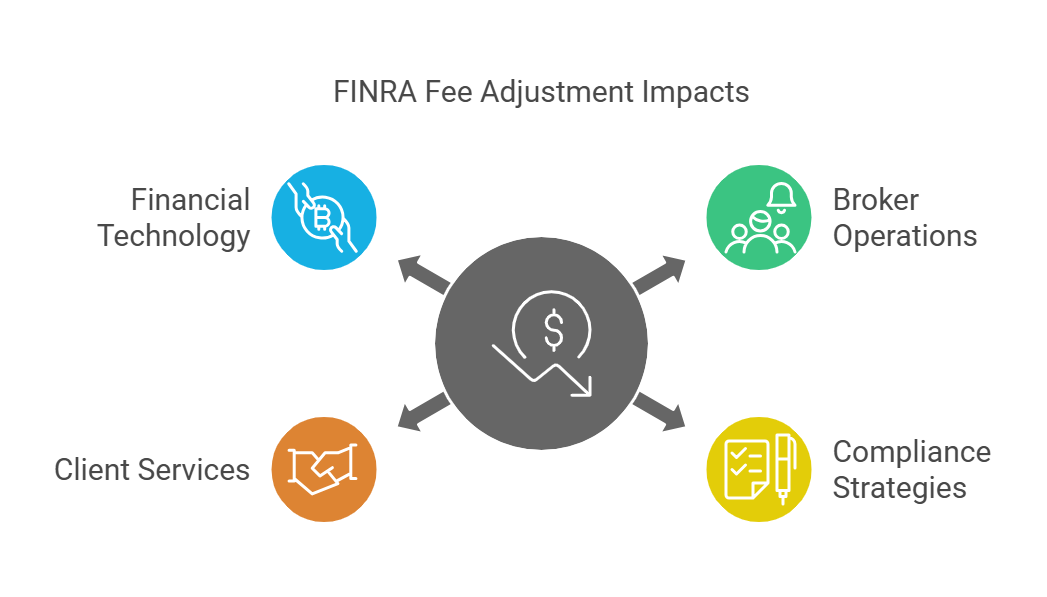

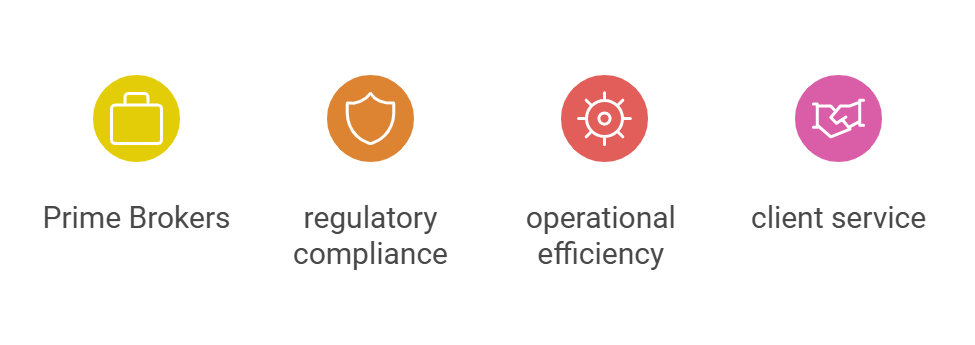

A Deeper Dive: Impact on Prime Brokers and Clearing Firms

For Prime Brokers:

For Prime Brokers:

- Strategic Compliance Management: The adjustments in fees underscore the pivotal role of prime brokers in ensuring meticulous compliance without bleeding resources. Prime brokers are at a juncture where leveraging technology can not only streamline regulatory adherence but also crystallize operational efficiencies.

- Client Service and Operational Agility: With an emphasis on maintaining market integrity, prime brokers need to juggle regulatory compliance and client service seamlessly. Here, innovative solutions provided by platforms like Loffa Interactive Group can be game-changers, enabling prime brokers to maintain agile operations while anchoring a client-centric approach.

For Executing/Clearing Brokers:

- Regulatory Compliance Navigating: Executing or clearing brokers face the direct brunt of such fee adjustments, given their critical role in trade execution and settlement. Adapting to these changes with technological aid can minimize disruptions and enhance compliance procedures, ensuring a smoother transaction flow.

- Operational Efficiency: The knack for keeping operational costs in check while adhering to regulatory mandates becomes paramount. Through adopting SaaS solutions like those offered by Loffa Interactive Group, executing and clearing brokers can fortify their compliance posture while optimizing operational workflows, saving both time and resources.

The Role of Technology: A Beacon of Adaptation

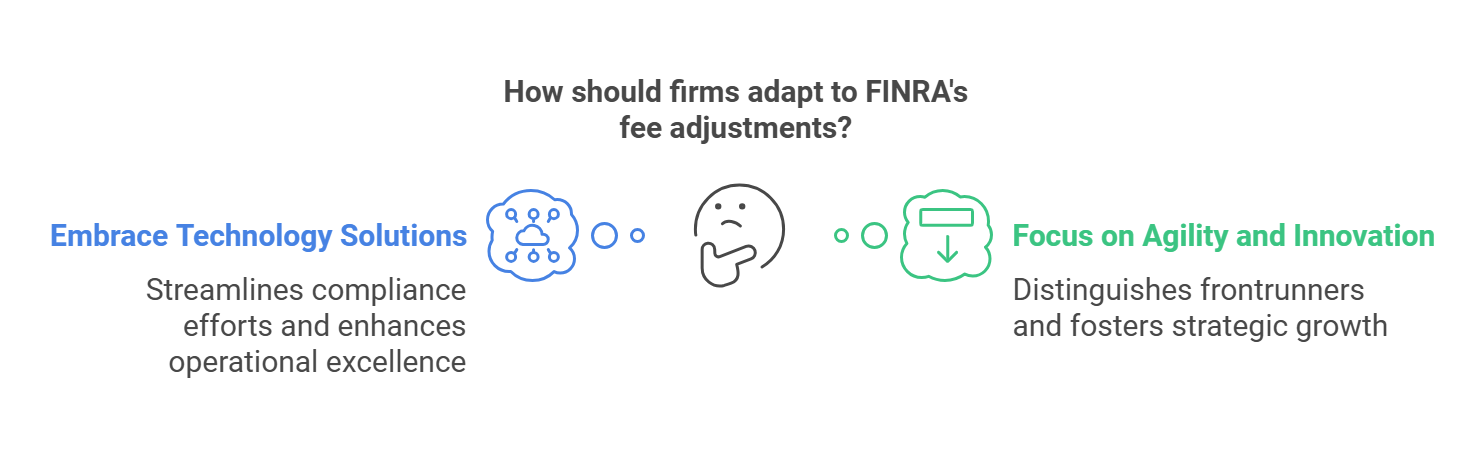

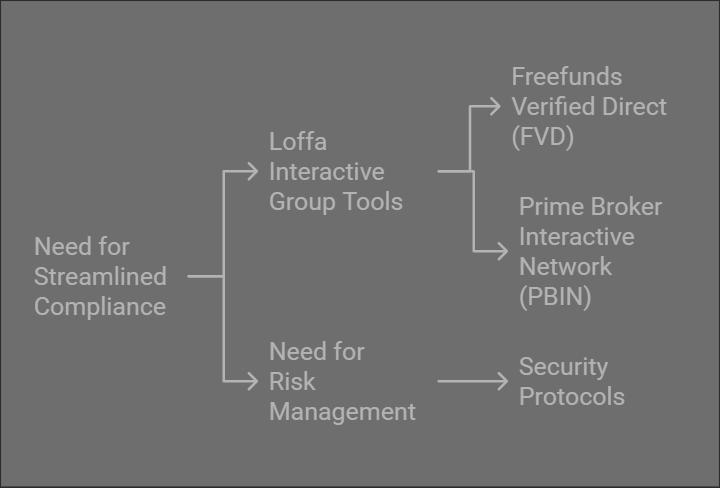

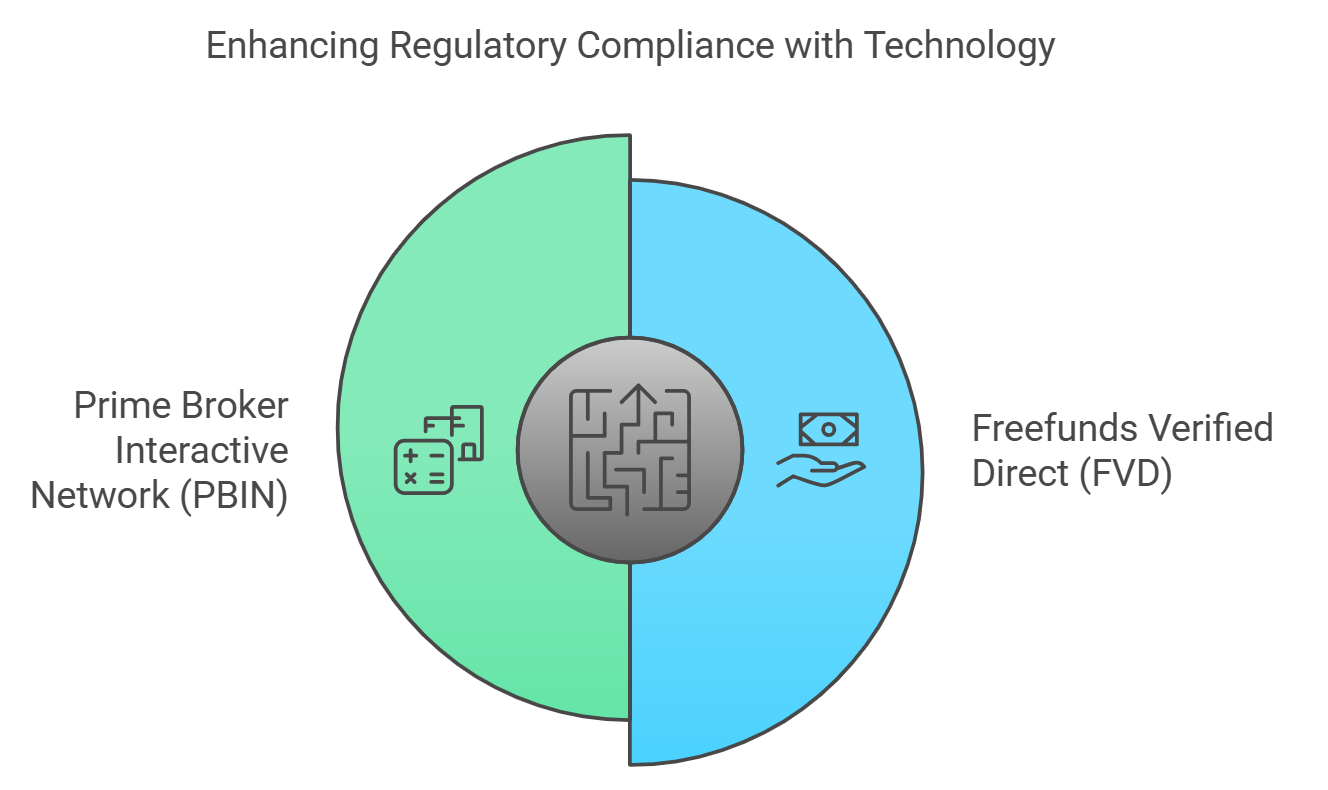

In anticipation of FINRA’s fee adjustments, evaluating and fortifying compliance frameworks becomes crucial for member firms. Loffa Interactive Group emerges as a steadfast ally in this endeavor, providing sophisticated tools such as Freefunds Verified Direct (FVD) and the Prime Broker Interactive Network (PBIN). By embracing these solutions, firms not only streamline compliance efforts but also edge closer to operational excellence amidst a cost-conscious landscape.

Embracing the Future

As we edge towards the implementation of FINRA’s fee adjustments, the agility to adapt and the willingness to innovate distinguish the frontrunners in the financial services industry. Collaboration with seasoned technology partners like Loffa Interactive Group equips firms to navigate these changes confidently, ensuring they not only meet the compliance threshold but also leverage it as a stepping stone to greater resilience and strategic growth.

In navigating the complexities of a changing regulatory environment, the adoption of advanced technology solutions offers a pathway to maintaining compliance, achieving operational efficiency, and ultimately securing a competitive advantage in the dynamic financial sector.

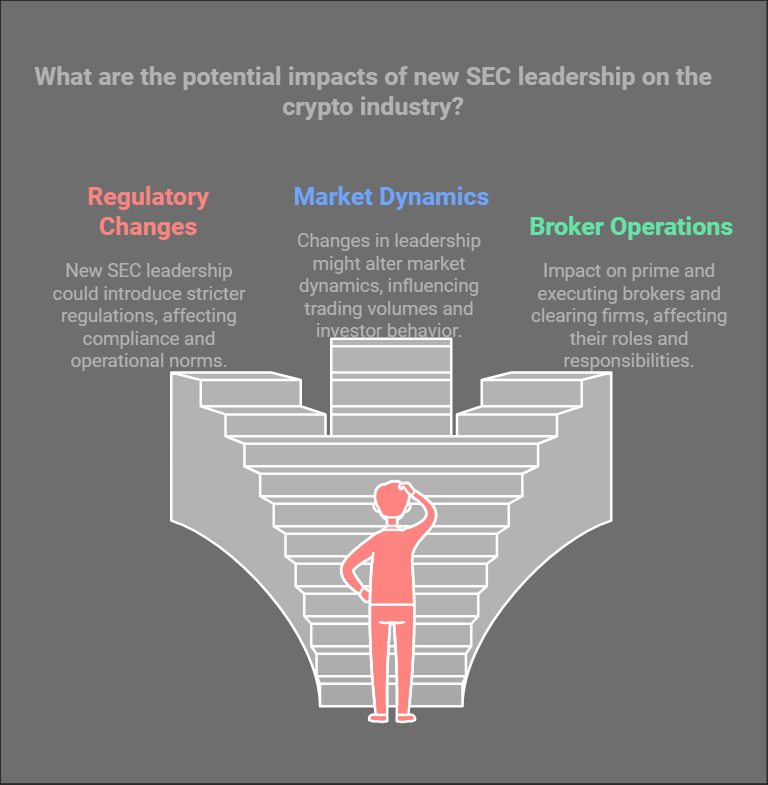

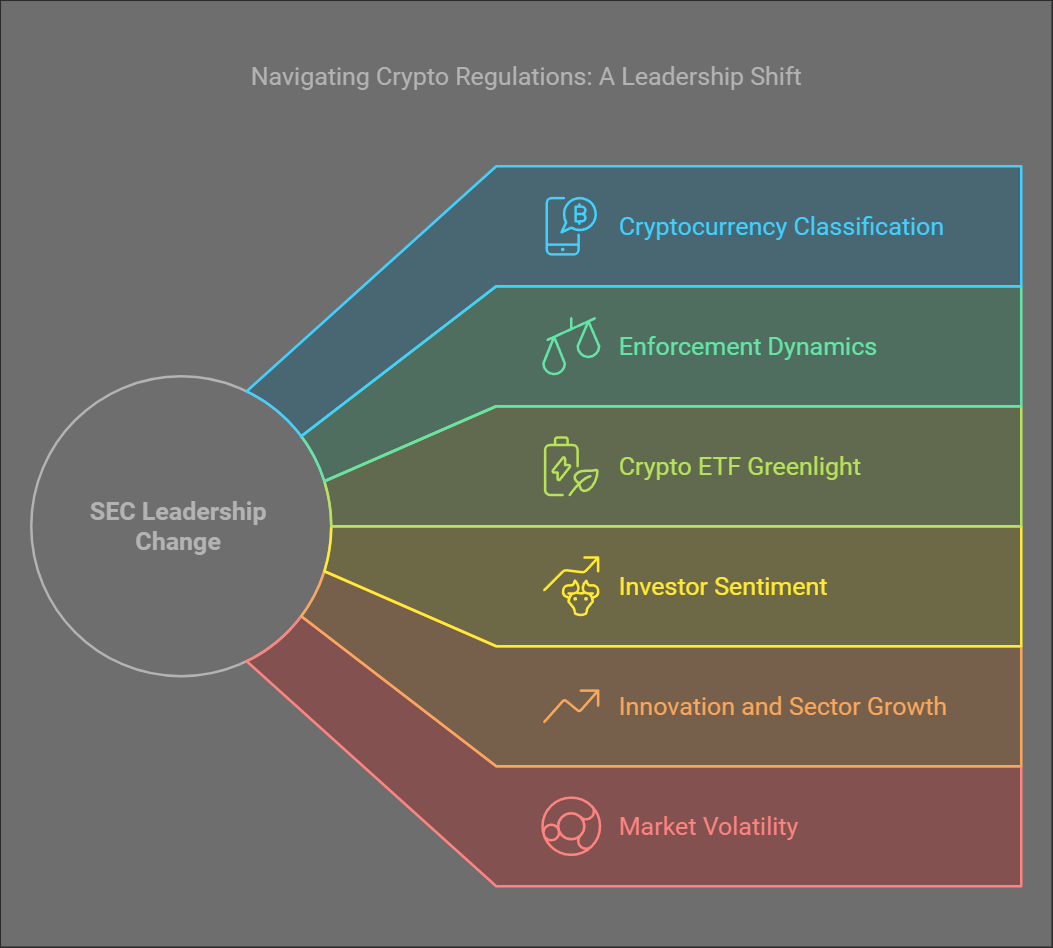

A novel leadership helm at the SEC portends a series of transformational shifts in crypto regulations:

A novel leadership helm at the SEC portends a series of transformational shifts in crypto regulations:

Loffa Interactive boasts a product suite designed to ease regulatory compliance burdens. With tools like Freefunds Verified Direct (FVD) and the Prime Broker Interactive Network (PBIN), Loffa enables firms to adeptly navigate the regulatory maze.

Loffa Interactive boasts a product suite designed to ease regulatory compliance burdens. With tools like Freefunds Verified Direct (FVD) and the Prime Broker Interactive Network (PBIN), Loffa enables firms to adeptly navigate the regulatory maze.